Catalog of SIP Cores

System on Chip design resources

System on Chip design resources

Embedded camera apps for automotive, tablets & PCs, phones, security & surveillance keep chip sales alive.

July 01, 2014 -- Almost as quickly as they took over, stand-alone digital cameras are now being displaced by camera-equipped cellphones, which have improved significantly in picture-taking quality and, more importantly, can immediately send copies of electronic photos by e-mail or post them on the Internet.

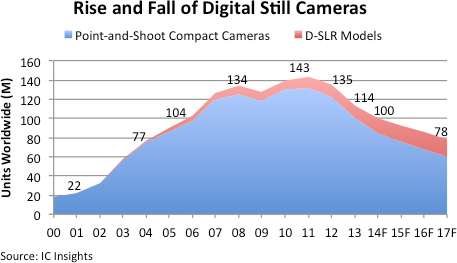

The decline in compact digital still camera shipments accelerated in 2013, causing most suppliers to reduce the number of models being sold to consumers and to focus more efforts on higher-priced digital single-lens reflex (D-SLR) cameras. Sales of D-SLR models are still growing but not by enough to keep the camera business from shrinking. Total digital still camera (DSC) shipments peaked in 2011 at 143 million units (Figure 1). Worldwide DSC shipments are expected to fall by a CAGR of -10% between 2012 and 2017 compared to an annual average growth rate of just 1% in the 2007-2012 period and nearly 31% per year in the 2002-2007 timeframe.

Figure 1

For many years, stand-alone DSC products drove advancements in digital imaging systems—including greater picture resolution in image sensors, more powerful camera processors, and higher density nonvolatile NAND flash memory. But the decline in stand-alone DSC shipments has caused a number of IC suppliers to shift strategies and seek out other expanding markets. Cellular phones continue to be a major growth application for digital cameras and imaging, but IC Insights predicts high growth rates for several other embedded applications this decade including automotive, tablets & PCs, security & surveillance, and medical/scientific/industrial, which will open high-volume market opportunities for image sensor suppliers and IC makers in the near future.

Figure 2 breaks out IC sales by type of camera application. IC sales for stand-alone digital cameras are projected to decline at an annual average rate of -10.5% in the forecast period, while revenues for integrated circuits used in automotive camera systems are expected to surge by a CAGR of 113.3% between 2012 and 2017. Sales of ICs for tablet and PC cameras are forecast to rise by a CAGR of 20.2% while cellphone camera integrated circuits are expected to rise by an annual rate of 9.0% in the 2012 2017 period.

Figure 2

Semiconductor suppliers stand to benefit from the migration of camera technology into a greater range of applications. The total IC market for all digital camera systems (embedded and stand-alone systems) is expected to reach $29.2 billion in 2017 compared to $23.0 billion in 2012, which represents a CAGR of 4.9%. When stand-alone cameras are excluded from these totals, IC sales for embedded cameras and imaging systems are forecast to grow by a CAGR of 11.9%, reaching $23.9 billion in 2017 compared to $13.6 billion in 2012.

Report Details: IC Market Drivers 2014

IC Market Drivers 2014—A Study of Emerging and Major End-Use Applications Fueling Demand for Integrated Circuits examines the largest, existing system opportunities for ICs and evaluates the potential for new applications that are expected to help fuel the market for ICs.

IC Market Drivers is divided into two parts. Part 1 provides a detailed forecast of the IC industry by system type, by region, and by IC product type through 2017. In Part 2, the IC Market Drivers report examines and evaluates key existing and emerging end-use applications that will support and propel the IC industry through 2017. Some of these applications include the automotive market, cellular phones (including smartphones), personal/mobile computing (including tablets), wireless networks, digital imaging, and a review of many applications to watch—those that may potentially provide significant opportunity for IC suppliers later this decade. The 2014 IC Market Drivers report is priced at $3,290 for an individual-user license and $6,390 for a multi-user corporate license.