Catalog of SIP Cores

System on Chip design resources

System on Chip design resources

Mar. 23, 2015 –

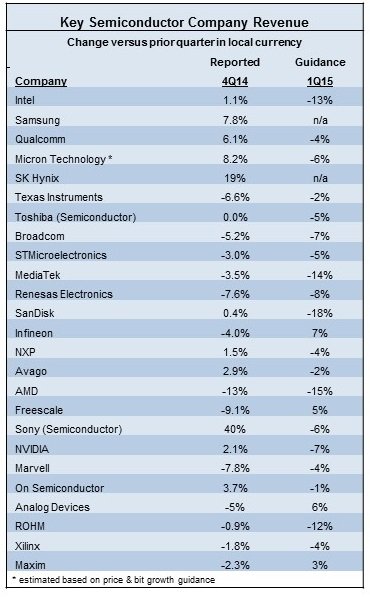

A weak first quarter outlook for the semiconductor market is indicating a slow start to 2015. Intel recently lowered the midpoint of its 1Q 2015 revenue guidance from $13.7 billion (down 7% from 4Q 2014) to $12.8 billion (down 13%). The table below shows the estimated top 25 semiconductor companies revenue change for 4Q 2014 versus 3Q14 and revenue guidance for 1Q 2015 versus 4Q 2014. Of the 23 companies providing guidance for 1Q 2015, only four (Infineon, Freescale, Analog Devices and Maxim) expect positive change from 4Q 2014. Five companies expect double digit declines (Intel, MediaTek, SanDisk, AMD and ROHM). Some of the reasons cited for the sluggish outlook are weak business PC demand (Intel), excess inventory in the channel (AMD and SanDisk), limited supply due to technology transitions (Micron), a smartphone market transition (MediaTek), and uncertainty in electronic markets and exchange rates (ROHM).

The average guidance is a 5.1% decline. The revenue-weighted average is minus 7.5%. Using the high end of each company’s revenue guidance for 1Q 2015 results in a revenue-weighted average minus 5.0%. Over the last five years, the semiconductor market 1st quarter change from the prior 4th quarter has ranged from a 3.7% increase to a 5.1% decline, averaging minus 1.0%. The market could potentially experience the worst 1st quarter decline since minus 16% in 1Q 2009 during the last major semiconductor downturn.

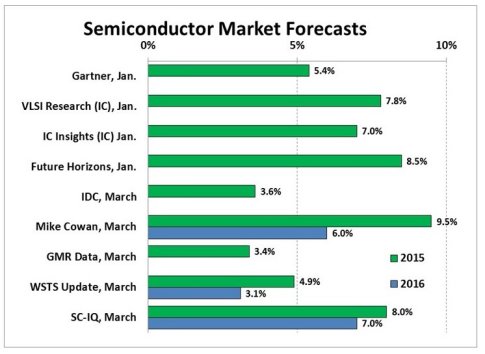

The outlook for the full year 2015 is varied. Forecasts since January fall into two general ranges: 3.4% to 5.4% (Gartner, IDC, GMR Data, and WSTS) and 7.0% to 9.5% (VLSI Research, IC Insights, Future Horizons, Mike Cowan and SC-IQ). The announced forecasts for 2016 range from 3.1% (WSTS) to 7% (our Semiconductor Intelligence or SC-IQ forecast). In December 2014, our SC-IQ forecast was 11% for 2015 and 7% for 2016. We have revised downward our expected growth for 2015 to 8% based on the projected weak 1Q 2015. We are keeping the 7% forecast for 2016.

Key assumptions are supporting healthy growth in 2015 and 2016 as shown in the table below. The International Monetary Fund (IMF) projects accelerating World GDP growth in 2015 and 2016. Gartner is forecasting accelerating growth in the combination of PC and tablet units. One area of concern is slowing growth rates for mobile phones and smartphones. Gartner expects total mobile phone unit shipment growth to pick up to 3.7% in 2015 from 1.7% in 2014, but slow to 3.3% in 2016. eMarketer projects slowing growth rates in smartphone users, from 25% in 2014 to 17% in 2015 and 13% in 2014.

| Annual Change | 2014 | 2015 | 2016 | Source |

| World GDP | 3.3% | 3.5% | 3.7% | IMF, Jan. |

| PC + Tablet units | 1.8% | 3.7% | 6.9% | Gartner, Jan. |

| Total mobile phone units | 1.7% | 3.7% | 3.3% | Gartner, Jan. |

| Smartphone users | 25% | 17% | 13% | eMarketer, Dec. 2014 |

Our forecast assumes solid growth for the key drivers of the semiconductor industry over the next few years. The trend from 9.9% in 2014 to 8% in 2015 and 7% in 2016 assumes moderating growth of some key drivers such as smartphones. Barring an economic downturn, the semiconductor market should experience average growth around 6% annually through the end of the decade.