Catalog of SIP Cores

System on Chip design resources

System on Chip design resources

Chinese IC companies held only 3% of total IC sales in 2015.

Apr. 05, 2016, Apr. 05, 2016 – IC Insights recently released its March Update to the 2016 McClean Report. The Update includes a review of IC company sales by headquarters location. In this example, Samsung's sales from its fabrication facility in Austin, Texas, are counted as sales from South Korean companies. Intel's sales from its fabs in China, Ireland, and Israel are included among U.S. companies, etc. As shown, U.S. companies held a 54% share of the total worldwide IC market in 2015, which includes sales from IDMs and fabless IC companies. The total does not include foundry sales. South Korean companies captured a 20% share of total IC sales and Japanese companies placed third with only an 8% share. Chinese companies accounted for just 3% of total IC sales last year (Figure 1).

The Taiwanese companies, on the strength of their fabless company IC sales, first surpassed the European companies in total IC sales share in 2013. However, although the European companies had about $1.4 billion less in total IC sales as compared to the Taiwanese companies last year, the European companies could surpass the Taiwanese companies in IC sales this year as Europe-headquartered NXP absorbs Freescale's $3.7 billion in IC sales as a result of their merger in December 2015.

As depicted in Figure 1, the South Korean and Japanese companies are extremely weak in the fabless IC segment with the Taiwanese and Chinese companies displaying a noticeable lack of presence in the IDM (i.e., companies with IC fabrication facilities) portion of the IC market. Overall, U.S.-headquartered companies show the most balance with regard to IDM, fabless, and total IC industry marketshare.

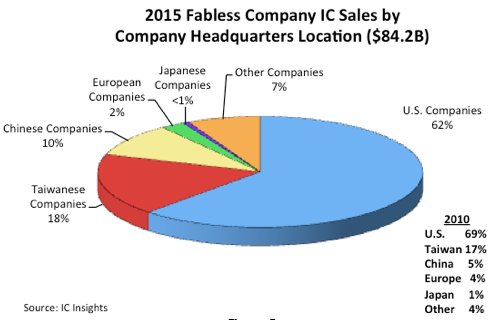

Figure 2 depicts the 2015 fabless company share of IC sales by company headquarters location. As shown, at 62%, the U.S. companies held the dominant share of fabless IC sales last year, although this share was down from 69% in 2010. Since 2010, the largest increase in fabless IC marketshare has come from the Chinese suppliers, which held a 10% share last year as compared to only 5% in 2010.

In contrast to the situation in the IDM segment, in which the European companies are expected to gain marketshare through acquisitions, the European fabless IC companies lost marketshare in 2015. The reason for this loss was the acquisition of U.K.-based CSR, the second largest European fabless IC supplier, by U.S.-based Qualcomm and the purchase of Germany-based Lantiq, the third largest European fabless IC supplier, by U.S.-based Intel in early 2015. These acquisitions left Dialog as the only Europe-headquartered fabless IC supplier in the top 50-company ranking and subtracted about $1.2 billion from the total European-headquartered fabless IC sales total, dropping their share to only 2% last year.

Figure 1

Figure 2

Report Details: The 2016 McClean Report

Further details on IC sales by region and by company, including IC Insights' final sales ranking of the top 50 IDM and top 50 fabless IC companies for 2015, are included in the March Update to The McClean Report - A Complete Analysis and Forecast of the Integrated Circuit Industry. A subscription to The McClean Report includes free monthly updates from March through November (including a 250+ page Mid-Year Report), and free access to subscriber-only webinars throughout the year. An individual-user license to the 2016 edition of The McClean Report is priced at $3,890 and includes an Internet access password. A multi-user worldwide corporate license is available for $6,890.

To review additional information about IC Insights' new and existing market research reports and services please visit our website: www.icinsights.com.

More Information Contact

For more information regarding this Research Bulletin, please contact Bill McClean, President of IC Insights. Phone: +1-480-348-1133, email: bill@icinsights.com